Mamdani Is About to Screw Up NYC Housing. Surprised?

The Great Gen Z Buyer’s Remorse: When “Vibes” Meet Macro-Prudential Reality

New York City just reran the St. Paul rent-control experiment — knowingly. Six weeks after Gen Z’s “decommodification” victory, capital is exiting, permits are collapsing, and maintenance math is breaking. This MacroMashup issue explains why deliberately making housing uninvestable freezes supply, why Minneapolis quietly produced better outcomes, and why state capacity — not moral intent — is the binding constraint in urban housing policy.

New York didn’t stumble into this.

In late 2025, Gen Z didn’t just post about power — they exercised it. City Hall flipped on a promise to “decommodify” housing, punish landlords, and make New York explicitly hostile to private capital.

Six weeks later, the dopamine high is fading.

What was sold as a moral reset of the “real estate power structure” is beginning to look familiar: collapsing asset values, disappearing permits, and lenders quietly stepping back. Even the language has shifted. Capital markets are now using the same word for NYC multifamily that Exxon once used for Venezuela.

Uninvestable.

This wasn’t an accident. It was a choice — and we’ve already seen how it ends.

Macro Context (Why This Matters Now)

Zoom out, and the timing isn’t random.

Inflation is cooling, but not collapsing

Labor is softening, not breaking

Gold is quietly reshaping trade flows

AI multiples deflated, but the capex cycle didn’t die

Against that backdrop, New York chose to test whether politics alone can suspend capital constraints.

History says it can’t.

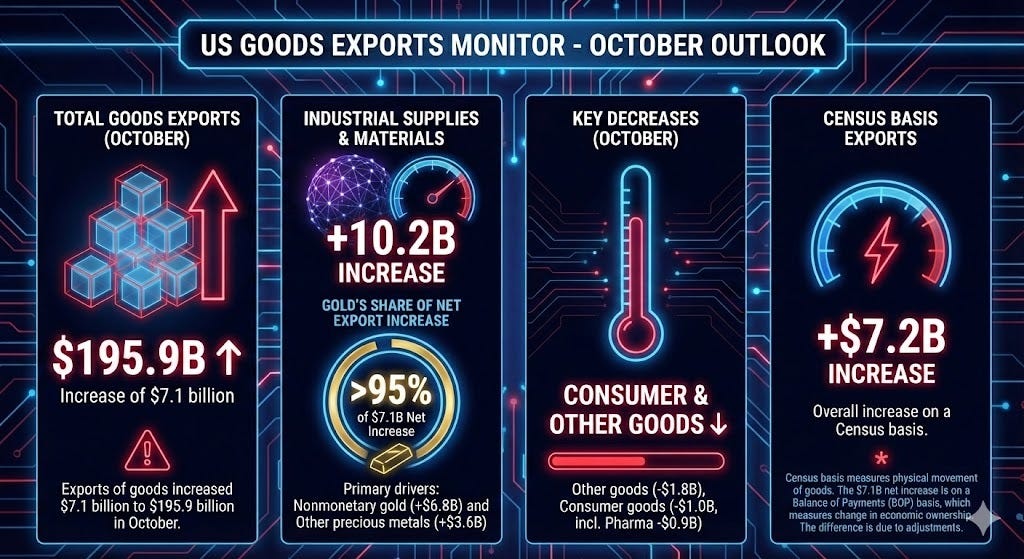

The Trade Deficit Mirage

October delivered a headline that looked like a breakthrough: the U.S. trade deficit collapsed to roughly $29 billion, a 16-year low and nearly a 40% improvement from September.

At first glance, it read like proof that industrial policy was working — factories humming, exports surging, America “making things” again.

That isn’t what happened.

The swing came almost entirely from a double-digit-billion spike in non-monetary gold exports and other precious-metal flows, not from a revival in manufactured goods. Strip those flows out, and the picture looks far more familiar.

That distinction matters. When precious metals move headline trade data, you’re no longer talking about competitiveness.

You’re talking about balance sheets.

This week, we go deeper into what those flows actually signal — and why metals, not machines, are quietly becoming the marginal asset class of this cycle.

Where This Goes Next

This is where the overview ends.

In the rest of this issue, we walk through:

Gen Z thought they were buying

What they’re actually getting

Why Minneapolis beat St. Paul

Why maintenance math always wins

Why state capacity is the real constraint

And why renters pay first when capital leaves

New here? Welcome! MacroMashup exists to connect policy, capital, and reality — before the consequences are obvious.

If you want to stay ahead of the next urban macro shift, this is where the work continues.

Paid subscribers get:

Full macro deep dives with the mechanics explained

Clear frameworks for interpreting policy, capital flows, and power

Early insight into regime shifts before they show up in prices

Access to members-only analysis and commentary

If you want to keep thinking in second-order effects — not narratives — this is where the real work continues.

Continue reading here →